23 November 2017

Inversión en América Latina a través de las ETVEs españolas / Spain: the Gateway to Latin America

Please click here for the English version

Las denominadas Entidades de Tenencia de Valores Extranjeros españolas, (“ETVE”) ofrecen importantes beneficios fiscales para inversores.

Estos beneficios vienen dados gracias a la amplia red de convenios para evitar la doble imposición (“CDI”) que España ha suscrito con Latinoamérica combinado con la utilización del régimen fiscal especial previsto en la normativa española para las ETVE.

Como resultado, los inversores pueden optimizar la tributación de las rentas y los dividendos procedentes de su participación en entidades residentes en países extranjeros. Esto hace de España una jurisdicción atractiva con grandes oportunidades para canalizar la inversión en Latinoamérica.

| 1. | Qué es una ETVE? |

El Régimen Especial de las ETVE (el “Régimen Especial”) se encuentra regulado en la Ley del Impuesto sobre Sociedades (“Ley del IS“[1]) y resulta interesante desde una doble perspectiva:

| a) | Facilita la distribución a España de rentas obtenidas en los países donde operan sus filiales, sin tener que tributar por ello en el Impuesto sobre Sociedades español. Estas rentas están normalmente exentas de retención en la fuente, o cuentan con una retención reducida, por aplicación de los CDI suscritos por España; y |

| b) | La distribución de dividendos por parte de la ETVE a su socio no residente o, la ganancia puesta de manifiesto con ocasión de la transmisión de las acciones de la ETVE, no se entienden obtenidos en territorio español, por lo que no se genera tributación en España. |

La aplicación del Régimen Especial conlleva la obtención de interesantes beneficios fiscales, sobre todo de cara al socio inversor no residente en España.

| 2. | Cuáles son los requisitos de la ETVE? |

| a) | Las ETVEs deben incluir en su objeto social la gestión y administración de participaciones en sociedades extranjeras que realicen actividades económicas en el extranjero y deben contar con los medios humanos y materiales necesarios para llevar a cabo dicho objeto; |

| b) | Las participaciones de la ETVE tienen que ser nominativas; y |

| c) | La creación de la ETVE y la aplicación del Régimen Especial tiene que ser notificada a la Agencia Tributaria Española. |

| 3. | Régimen fiscal de la ETVE |

| 3.1 | Rentas obtenidas por la ETVE: |

Las rentas obtenidas por la ETVE, procedentes de participaciones, están sujetas al régimen de exención general previsto en la Ley del IS, aplicable a todas las sociedades sujeto pasivo del impuesto, con sus mismos requisitos:

Como regla general, los dividendos y las ganancias de fuente extranjera están exentos si:

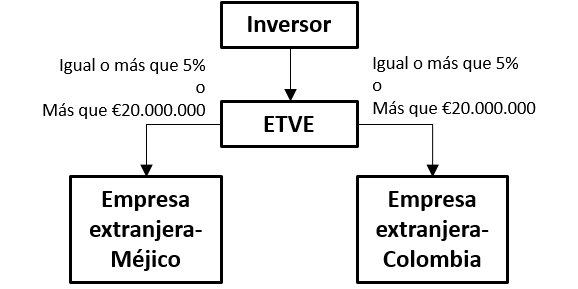

| (i) | El porcentaje de participación es igual o mayor al 5%, o su valor de adquisición es superior a 20.000.000 euros, y se ha mantenido durante al menos un año; y |

| (ii) | La entidad participada ha estado sujeta y no exenta a un impuesto de naturaleza idéntica o análoga al IS español, a un tipo nominal de al menos el 10%. |

Las rentas obtenidas a través de un Establecimiento Permanente (“EP”) están exentas si:

| (i) | El EP está sujeto y no exento a un impuesto de naturaleza idéntica o análoga al IS español, a un tipo nominal de al menos el 10%. |

| 3.2 | Rentas distribuidas por la ETVE en forma de dividendos: |

Si los dividendos se distribuyen a:

| a) | Socios no residentes: No hay tributación en España (se considera que la renta no se ha obtenido en España) salvo:

(i) Dividendos procedentes de rentas no exentas bajo la Ley del IS; (ii) Socio residente fiscal en paraíso fiscal. |

| b) | Socios personas jurídicas residentes: Tratamiento general de acuerdo con la Ley del IS (posible aplicación de exención por doble imposición interna si se cumplen los requisitos para ello); |

| c) | c) Socios personas físicas residentes: Tributación en el Impuesto de la Renta sobre la Personas Físicas (“IRPF”), en la base del ahorro (a un tipo del 19%-23%). |

| 3.3 | Rentas obtenidas por los socios de la ETVE en forma de plusvalía: |

Si las rentas obtenidas derivan de la venta de participaciones en la ETVE:

| a) | Por socios no residentes: No hay tributación en España, salvo:

(i) Plusvalía imputable a activos distintos de participaciones en entidades no residentes exentas; (ii) Socio residente fiscal en paraíso fiscal. |

| b) | Por socios personas jurídicas residentes: Exención de la ganancia obtenida, siempre que se cumplan los requisitos previstos a estos efectos en la Ley del IS. |

| c) | Por socios personas físicas residentes: Tributación en el IRPF en la base del ahorro (a un tipo del 19%-23%). |

| 4. | América Latina y el potencial de las ETVEs como vehículo de inversión |

Como se ha apuntado, una de las grandes ventajas de las ETVEs es la ausencia de tributación en España en la repatriación a los socios no residentes de las rentas obtenidas en sus inversiones extranjeras. Adicionalmente, al ser la ETVE una sociedad residente en territorio español, puede acogerse a los beneficios previstos en los CDIs firmados por España.

En la actualidad, y por lo que respecta a América Latina, España cuenta con 14 CDIs en países latinoamericanos: Argentina, Bolivia, Brasil, Chile, Colombia, Costa Rica, Cuba, Ecuador, El Salvador, México, Panamá, República Dominicana, Uruguay y Venezuela.

El MSCI Emerging Markets Index, también conocido como el ponderador estadounidense de fondos de capital de inversión, ha identificado en el 2017 a Brasil, México, Colombia y Chile como países con economía emergente en Latinoamérica. Estos países contienen un carácter potencial para la inversión extranjera debido a su creciente apertura al capital extranjero y a la situación económica con un grado importante de liberalización.

En definitiva, España a través del Régimen Especial de las ETVEs y de su extensa red de convenios, se ha convertido en una jurisdicción muy interesante para canalizar inversiones en distintos países latinoamericanos logrando una optimización de la eficiencia fiscal de dichas inversiones.

Spain: the Gateway to Latin America

The use of Spanish holding companies to invest in Latin America (“LATAM”) offers a number of tax benefits for investors.

These benefits come from the use of double taxation treaties (“DTT”), combined with a special tax regime in Spain for holding companies (the “ETVE Regime”). Holding companies taxed under the ETVE Regime are known as ETVEs.

As a result, channeling investments into LATAM countries through a Spanish holding allows the optimization of the taxation on income and profits distributed from a LATAM subsidiary.

| 1. | What is the ETVE Regime? |

The Spanish Corporate Income Tax Law (“CIT Law”) foresees a special tax regime for holding companies, the ETVE Regime, which provides for tax benefits at the level of both the Spanish ETVE, and its shareholder. This special regime is particularly favorable to non-Spanish tax resident investors:

| a) | Taxation of income at the level of the Spanish holding company or ETVE: income (dividends and capital gains) derived by the Spanish holding company from its foreign subsidiaries is exempt from Spanish Corporate Income Tax (“CIT”), provided certain conditions are met. Further, dividends are usually exempt from withholding tax or, can benefit from a reduced withholding tax, in the source state, pursuant to the DTT entered into with Spain and the jurisdiction of the tax residence of the subsidiary paying the dividends. |

| b) | Taxation of income at the level of the non-Spanish tax resident investor: dividends distributed by the ETVE (out of income generated by the LATAM subsidiaries) to the non-Spanish tax resident investors are not considered as obtained in Spain, and are thereby not subject to Spanish taxation. |

| 2. | What are the requirements for the ETVE? |

| a) | The company’s corporate purpose must include the management and control of participations of non-resident subsidiaries through proper human and material resources; |

| b) | The ETVE shares must be nominative; and |

| c) | The application of the ETVE regime must be notified to the Spanish Tax Authorities. |

| 3. | ETVE’s Tax Regime |

| 3.1 | Income obtained by ETVE: |

The Spanish CIT Law foresees a participation exemption regime for dividends and capital gains applicable to all CIT taxpayers who meet the relevant requirements. Dividends and capital gains obtained by the ETVE can also benefit from such general exemption.

As a general rule, foreign dividends and capital gains are exempt from Spanish CIT if:

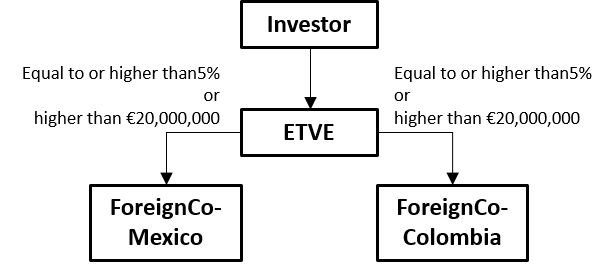

| (i) | The percentage of shareholding is at least 5%, or the acquisition value of the shareholding is over €20,000,000, and it has been maintained for at least one year; and |

| (ii) | The subsidiary is subject to an identical or similar CIT with a nominal tax rate of at least 10%. This condition is deemed as met where there is a DTT between the jurisdiction of tax residence of the relevant subsidiary and Spain. |

Income obtained through a foreign Permanent Establishment (“PE”) is exempt if:

| (i) | The PE is subject to a similar or identical CIT with a nominal tax rate of at least 10%. This condition is deemed as met where there is a DTT between the jurisdiction in which the PE is located and Spain. |

| 3.2 | Dividends paid by the ETVE |

If dividends are paid:

| a) | To non-Spanish tax resident shareholders: there is no taxation in Spain (it is considered as income not obtained in Spain) except for:

(i) Dividends derived from non-exempt income (under the Spanish participation exemption regime); or (ii) Dividends paid to a shareholder with tax residence in a tax haven. |

| b) | To Spanish tax resident corporate shareholders: exemption under the Spanish participation exemption regime, provided all relevant conditions are met. |

| c) | To Spanish tax resident individual shareholders: subject to Spanish Personal Income Tax (“PIT”), as savings income[2] (at a 19%-23% tax rate). |

| 3.3 | Capital gains from the sale of ETVE shares |

If capital gains are derived from the sale of ETVE shares:

| a) | By non-Spanish tax resident shareholders: there is no taxation in Spain, except for:

(i) Capital gains allocated to assets others than those related to exempted foreign shareholdings; or (ii) Shareholders with tax residence in a tax haven. |

| b) | By Spanish tax resident corporate shareholders: exemption under the Spanish participation exemption regime, provided all relevant conditions are met; |

| c) | By Spanish tax resident individual shareholders: subject to PIT as savings income (at a 19%-23% tax rate). |

| 4. | LATAM and the potential of ETVEs as Investment Vehicles |

The greatest value of ETVEs for non-Spanish tax resident investors with shareholdings in LATAM subsidiaries is the mitigation of taxation in the repatriation of income obtained from their foreign investments under the ETVE Regime. In addition, the ETVE is a Spanish tax resident company, which is entitled to benefits provided under the DTTs signed by Spain with LATAM jurisdictions.

As of today, Spain is a signatory to 14 double tax treaties with LATAM countries comprising: Argentina, Bolivia, Brazil, Chile, Columbia, Costa Rica, Cuba, Dominican Republic, Ecuador, El Salvador, Mexico, Panama, Uruguay and Venezuela.

In 2017, the MSCI Emerging Markets Index, identified Brazil, Mexico, Columbia and Chile as emergent economies. As such, these countries offer potentially attractive investment opportunities. There also exists a greater liberalization of trade and higher level of convergence in terms of regulations within these economies. These are the key factors in considering the potential for LATAM future investments.

Through the use of the ETVE regime and DTTs, Spain renders itself as an attractive jurisdiction in order to channel investments into LATAM countries.

Disclaimer

Esta nota no es exhaustiva ni cubre todos los aspectos de las referidas normas, sin que haya sido redactada para prestar asesoramiento jurídico, fiscal o de otro tipo.

Esta nota está realizada por Anaford AG teniendo en cuenta la legislación vigente en el momento de su publicación.

This alert is not exhaustive and does not cover every single aspect of referred laws. The information provided in this alert should not be construed as legal advice or legal opinion regarding any specific facts or circumstances.

This alert was provided by Anaford AG, who have taken all reasonable care to ensure that the information contained in this alert is accurate at the time of publication.